As the Federal Emergency Management Agency’s future hangs in the balance, cities and states are taking on more responsibility for disaster preparedness and recovery. And even in this era of tight municipal budgets, now is not the time to reduce preparedness spending, research from Allstate, the U.S. Chamber of Commerce and its foundation found.

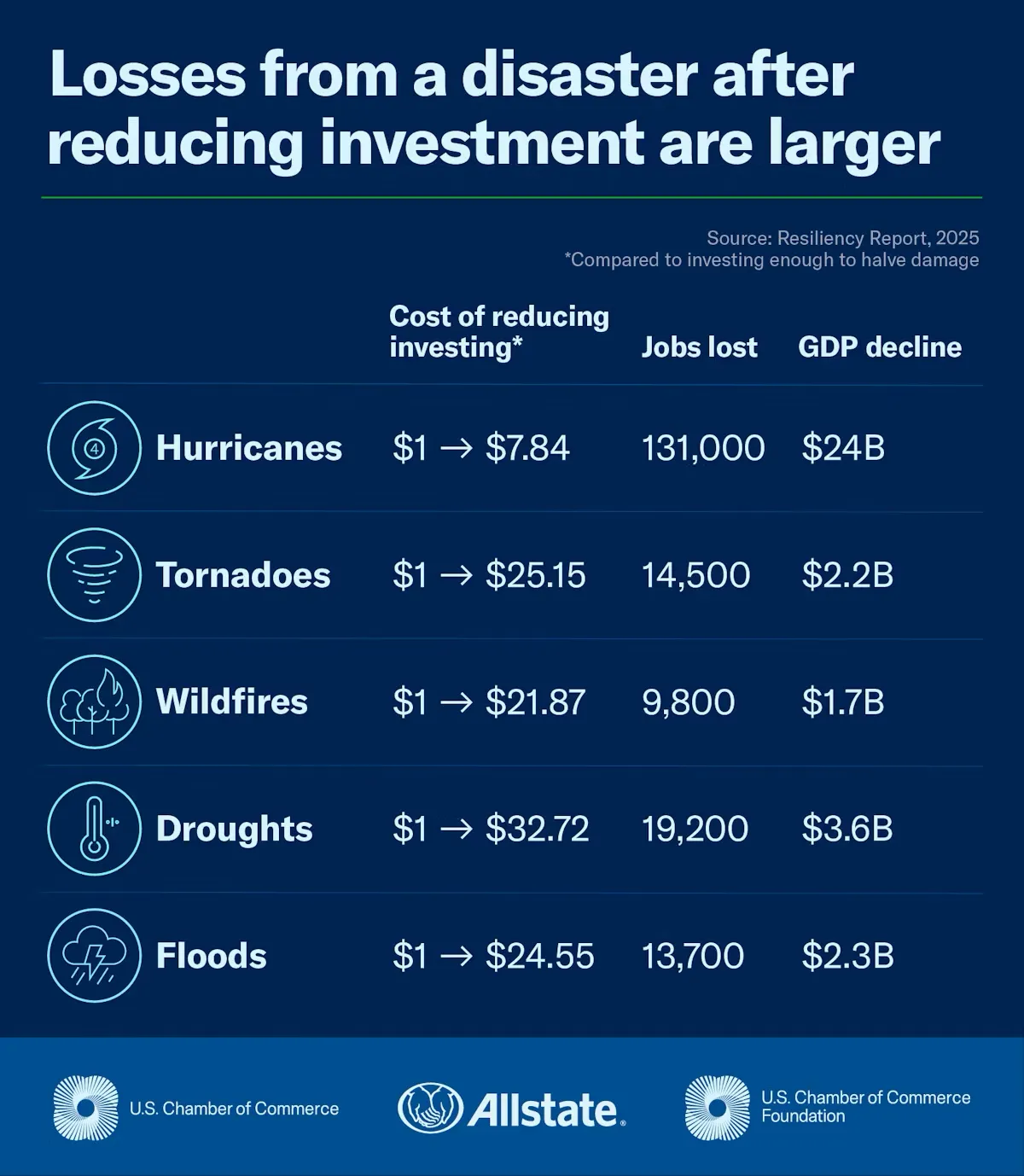

Every dollar not invested in disaster resilience today could result in up to $33 of lost future economic activity after a disaster, according to “Beyond the Payoff: How Investments in Resilience and Disaster Preparedness Protect Communities.” Furthermore, the research found that resilience funding stabilizes local labor markets. In hurricane-prone areas, it can prevent the loss of more than 70,000 jobs.

“Before now, no one’s really put a dollar figure to this — where there is a return on investment,” Marc DeCourcey, senior vice president of the U.S. Chamber of Commerce Foundation, told Smart Cities Dive. “Preparedness seemed like a good thing to do, but how do you quantify it? That’s where we dug in — and we made some really remarkable discoveries that it’s not just about physical damages, but it’s also economic impact. And that’s the real eye-opener.”

“For local towns and communities and cities, the message that has to get through is that these are investments in the economy,” Rich Loconte, senior vice president of government and industry relations at Allstate, told Smart Cities Dive.

A survey of emergency managers, risk professionals and state and local officials conducted for the report found that only 15% believe the U.S. is “very prepared” to manage a typical disaster. Half of the respondents said resilience efforts between the public and private sectors are poorly coordinated, and 59% said clearer processes and better resource allocation would have the greatest impact on improving those partnerships.

DeCourcey said his first piece of advice for local community leaders is to engage the business community in disaster preparedness. “It’s in their self-interest, too,” he said.

“This isn’t any one sector’s responsibility,” Loconte said. “It has to happen across the board. We have to have a broad coalition of partners in order to effect change.”

Investment opportunities

The report outlined six “levers of resilience” that communities should invest in to maximize the impact of their disaster preparedness spending:

1. Risk-informed design. Adopt and enforce hazard-resistant building codes, improve access to risk data and incentivize compliance to reduce structural vulnerability and long-term recovery costs.

2. Infrastructure and pre-disaster mitigation. Modernize infrastructure using resilient design principles and nature-based solutions and integrate resilience into capital improvement planning to minimize service disruptions and reduce response costs. Every dollar invested in mitigation can save an average of $6 in future disaster costs, according to the report.

3. Economic continuity and diversification. Support small business resilience and contingency planning, expand insurance coverage, invest in workforce development and strengthen supply chains to enhance economic stability and accelerate recovery.

4. Governance and cross-sector leadership. Establish mutual aid agreements, streamline interagency coordination and align resilience strategies with local priorities to improve operational efficiency and ensure cohesive disaster response and recovery.

5. Civic engagement. Launch public awareness campaigns, engage community-based organizations and promote household-level preparedness to build trust, strengthen social cohesion and empower communities to act.

6. Performance measurement and accountability. Implement resilience scorecards, conduct risk modeling and integrate performance metrics into planning and budgeting to support evidence-based decision-making and demonstrate return on investment.